Are you in the market to buy a new home? If so, you’ve probably heard the terms “prequalified” and “preapproved” thrown around. While they may sound similar, they have significant differences that can impact your home-buying process.

In this article, we’ll discuss pre-qualified vs pre-approved for home buyers. We’ll explain what each term means, how they differ, and which option is the best fit for you. Whether you’re a first-time homebuyer or a seasoned pro, understanding these terms is crucial to make informed decisions when it comes to financing your dream home. So, let’s get started!

What Does Pre-Qualification Mean?

Pre-qualification is an initial step in the home-buying process, where a lender assesses your financial situation to determine the amount of money they’re willing to lend you.

Essentially, pre-qualification helps you understand how much house you can afford before you start looking for one. It’s a great way to get an idea of what price range to search for and what your monthly mortgage payments might look like.

To get pre-qualified, you’ll need to provide basic information about your income, assets, and debts to the lender. This information is provided through a short online form, phone call, or in-person meeting. When seeking to get pre-qualified, make sure to have your driver’s license, recent pay stubs, W-2 and other tax forms, credit info, and bank statements at the ready.

The lender analyzes all of this information to determine your debt-to-income ratio (DTI), a comparison of your monthly debt payments to your monthly income. They will then provide you with an estimated loan amount that you may qualify for based on your DTI.

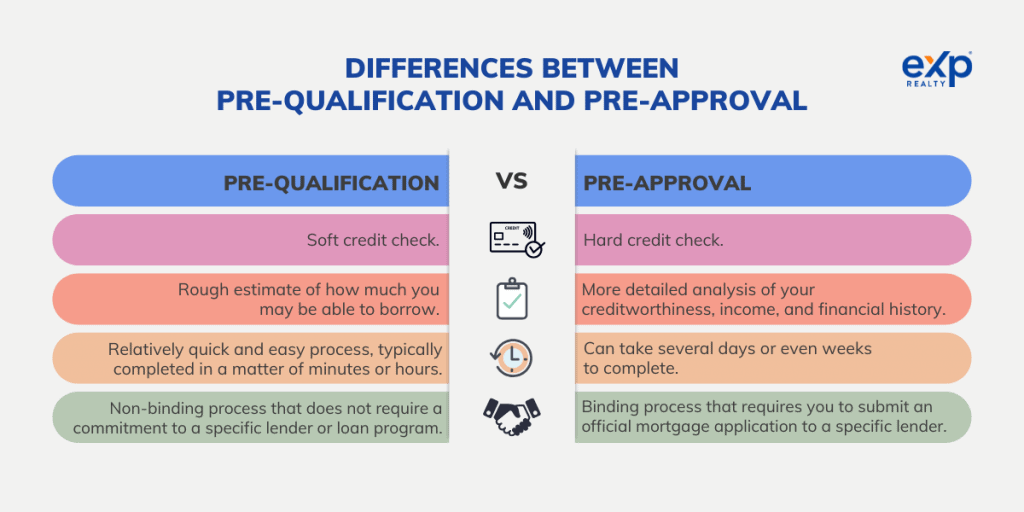

Pre-qualification is not a financing guarantee or a commitment to lend you money. It’s simply a rough estimate of how much you may be able to borrow based on the information you’ve provided.

What Does Pre-Approval Mean?

Pre-approval is a more formal process than pre-qualification. This is where a lender thoroughly evaluates your financial history, credit score, and current financial situation to determine how much they’re willing to lend you for a mortgage.

To get pre-approved, you’ll need to fill out a detailed application and provide supporting documentation such as bank statements, tax returns, pay stubs, and proof of assets. The lender will conduct a credit check and verify the information you’ve provided to determine your creditworthiness and ability to repay the loan.

Once the lender has evaluated your application and supporting documentation, they’ll issue a pre-approval letter that outlines the maximum loan amount you’re eligible for, the interest rate, and other loan terms. This pre-approval letter is usually valid for a certain period, typically 60 to 90 days.

Pre-approval is not a guarantee of financing, it simply shows you can get financing. You’ll still need to complete a full mortgage application and undergo additional underwriting before a loan is finalized.

Differences Between Pre-Qualification and Pre-Approval

In prequalification, the lender only conducts a primary evaluation of your financial situation based on the information you provide to verify your income and employment history. These include bank statements, tax returns, and pay stubs. The lender relies on the accuracy of the information you provide and doesn’t check it.

In contrast, the pre-approval process involves a more thorough evaluation of your financial situation. The lender will verify the provided information by checking your credit report, income, assets, and debts. It helps the lender ensure they have an accurate picture of your finances before making a loan offer.

Credit Check

When you apply for prequalification, the lender will conduct a soft credit check, which does not affect your credit score. It’s a quick and easy way for lenders to get a general idea of your creditworthiness without conducting a deep dive into your credit history.

On the other hand, during the pre-approval process, the lender conducts a hard credit check. It involves a more thorough review of your credit history and can indicate to credit reporting agencies that you’re actively seeking credit, which can impact your credit score for a short period.

During the preapproval process, the lender will review your credit report in detail to assess your creditworthiness and ability to repay the loan. They’ll look at factors such as your payment history, outstanding debts, and length of credit history. The lender uses the information to determine your credit score, calculate the interest rate, and your eligibility for other loan terms.

Accuracy of Assessment

Prequalification provides a rough estimate of how much you may be able to borrow, based on the information you provide to the lender. This preliminary assessment does not involve a detailed analysis of your creditworthiness, employment history, or financial situation. It’s therefore not as accurate as a preapproval.

In contrast, preapproval involves a more detailed analysis of your creditworthiness, income, and financial history. The lender will verify the information you provide and will also look at your credit report to assess your creditworthiness. Based on this information, the lender will give you a more accurate estimate of how much you can borrow and what interest rate you can expect.

Timeframe

Prequalification is a relatively quick and easy process, typically completed in a matter of minutes or hours. Since prequalification only involves a rudimentary evaluation of your financial situation based on the information you provide to the lender, it does not take long to complete.

On the other hand, pre-approval can take several days or even weeks to complete. It involves a more thorough evaluation of your financial situation, including a detailed analysis of your credit history, income, and assets.

Commitment

Prequalification is a non-binding process that does not require a commitment to a specific lender or loan program. It simply gives you a general idea of how much you may be able to borrow and what your monthly payments may look like. It allows you to shop around for the best offer without any rush.

In contrast, pre-approval is a more formal and binding process that requires you to submit an official mortgage application to a specific lender. This application is subject to approval, and once you’re pre-approved for a loan, you’re typically committed to working with that lender for a certain period, usually around 90 days.

During this time, you’re expected to find a home and complete the purchase process. If you decide not to go through with the purchase or choose to work with a different lender, you’ll need to go through the pre-approval process again with a new lender.

How Pre-Qualification and Pre-Approval Affect Homebuyers

Below are some ways that pre-qualification and pre-approval can affect homebuyers.

Understanding Your Budget

Pre-qualification and pre-approval help homebuyers understand how much they can afford to spend on a home. Pre-qualification provides a rough estimate, and pre-approval shows a more accurate assessment of your borrowing power. This information can help you focus your search on homes that fit within your budget.

Strengthening Your Offer

Pre-approval can give homebuyers an advantage when making an offer on a home. A pre-approval letter shows the seller you are a serious buyer who has already been approved for a loan. This can make your offer more attractive and increase your chances of being accepted in a competitive real estate market.

Streamlining The Home Buying Process

Pre-approval can also help streamline the home-buying process. Since you’ve already been approved for a loan, you can move quickly through the process once you find a home you want to buy. This can help you avoid delays and close on the house more quickly.

Avoiding Disappointment

Pre-qualification and pre-approval can also help you avoid disappointment later in the home-buying process. If you wait until you find a home you want to buy before seeking pre-approval, you may find out that you’re not able to get the financing you need. This can be disappointing and may cause you to miss out on your dream home.

Saving Money

Pre-approval can also help you save money in the long run. By getting pre-approved for a mortgage, you’ll better understand the interest rate you can expect and can shop around for the best deal. This can save you thousands of dollars over the life of your mortgage.

How Pre-Qualification and Pre-Approval Affect Homeowners

Pre-qualification and pre-approval are typically associated with the home-buying process, rather than homeownership itself. However, there are some ways that these processes can affect homeowners:

Refinancing

If you’re a homeowner looking to refinance your mortgage, pre-approval can be a helpful step. By getting pre-approved for a new mortgage, you’ll better understand your borrowing power and can shop around for the best deal.

Home Equity Loans And Lines Of Credit

Homeowners interested in taking out a home equity loan or line of credit may also find pre-approval processes helpful. A pre-approval gives you a better understanding of your borrowing power. It also allows you to shop around for a better deal.

Home Renovations

Homeowners planning to renovate their homes may find pre-qualification and pre-approval helpful. These processes can give you a better understanding of your borrowing power and help you determine how much you can afford to spend on your renovation project.

Home Equity

Pre-qualification and pre-approval can also affect your home equity. If you’re pre-approved for a new mortgage or home equity loan, you’ll be raising your debt and reducing your home equity. On the other hand, if you’re pre-approved for a lower interest rate or better terms, you may be able to increase your home equity over time by paying your mortgage more quickly.

How Pre-Qualification and Pre-Approval Affect Sellers

Sellers are more likely to accept an offer from a pre-approved buyer. Pre-approval demonstrates that the buyer is a serious contender who is likely able to secure the necessary financing to complete the transaction.

Streamlining The Sale Process

Pre-approval means the buyer has already completed much of the paperwork necessary to secure a mortgage. This means the sale process can be streamlined and expedited, potentially leading to a quicker closing.

Avoiding Potential Setbacks

If a buyer has not been pre-approved and their mortgage application is denied later in the process, the sale may be delayed or even fall through. Pre-approval can help avoid these potential setbacks and ensure a smoother sale process.

Reducing Risk

Pre-approval can also help reduce the risk of a sale falling through due to financing issues. This can be especially vital in a competitive real estate market where multiple offers may be received.

Key Takeaways

Pre-qualification and pre-approval are essential steps for all parties involved in the home-buying process, including buyers, sellers, and even homeowners looking to refinance or take out a home equity loan.

These processes can help buyers understand their borrowing power, identify potential roadblocks early on, and avoid setbacks later. For sellers, pre-approval can make their homes more attractive to serious buyers and streamline the sale process.

All parties can enjoy a smoother, more efficient, and less stressful home-buying experience by taking advantage of pre-qualification and pre-approval. If you’re interested in learning more, contact a local real estate agent.

FAQs

To help you further understand the difference between the prequalification and pre-approval processes, we have compiled and answered related FAQs from Google and forums.

Which is better pre-qualified or pre-approved?

Pre-approval is generally considered better than pre-qualification as it involves a more rigorous assessment of a buyer’s financial situation, including a credit check and verification of income and assets. Pre-approval can give buyers a more accurate idea of their borrowing power and make their offers more attractive to sellers.

Does pre-qualified mean approved?

No, pre-qualified does not mean approved. Prequalification is an initial assessment of your financial situation, allowing you to move to the pre-approval step. Pre-approval is a more in-depth review of your financial and employment status and background to determine if you actually qualify for the mortgage loan.

Does your credit go down from getting pre-qualified for a loan?

No, getting pre-qualified for a loan does not negatively impact your credit score. Pre-qualification typically involves a soft credit check, which does not affect your credit. However, pre-approval usually involves a hard credit check, which can cause a temporary dip in your credit score.

How long is pre-qualification good for?

Prequalification is typically only valid for a short period, usually around 60-90 days. After this time, the lender may require the borrower to update their financial information and undergo the prequalification process again to ensure that their financial situation has not changed.

What credit score is needed for pre-approval?

The credit score needed for pre-approval varies depending on the lender and type of mortgage. Generally, a credit score of 620 or higher is required for conventional mortgages. FHA loans may have lower credit score requirements.

Why is it important to get pre-qualified?

Getting prequalified for a mortgage helps you understand how much you can afford to borrow. This can help you focus your home search and avoid wasting time on properties outside your price range.

Does a pre-approval letter mean you are approved?

No, a pre-approval letter does not guarantee approval for a mortgage loan. It is a preliminary assessment of your creditworthiness based on the documentation you provide the lender. Final approval of the loan is contingent upon you meeting all underwriting requirements and providing updated documentation.

Can you be denied after pre-qualification?

Yes, you can be denied after pre-qualification. Pre-qualification is a preliminary step that provides an estimate of your borrowing power based on self-reported information. Your actual ability to secure a mortgage will depend on factors such as credit history, employment, and income. These are verified during the pre-approval process.

Can you put an offer in with a prequalification?

Yes, you can put an offer in with a prequalification. However, it may not carry as much weight as an offer backed by a pre-approval. Prequalification is an estimate of your borrowing power, while pre-approval involves a more thorough evaluation of your financial situation by a lender and thus carries more weight to home sellers.

Does getting multiple pre-approvals hurt your credit?

Getting multiple pre-approvals for a mortgage within a short period generally will not damage your credit score. The credit bureaus recognize you’re likely shopping around for the best deal and will often treat multiple inquiries made within a specific timeframe as a single inquiry.

What do they look at for prequalification?

For prequalification, lenders look at your basic financial information, such as your income, debt, and assets, to determine your general borrowing power and the types of loans you may qualify for. This process does not involve a credit check or in-depth verification of your financial information.